Python第6次作业

使用”数据4.3”数据文件(详情已在第4章习题部分中介绍),Profit contribution为利润贡献度,作为响应变量;Net interest income为净利息收入、Intermediate income为中间业务收入、Deposit and finance daily为日均存款加理财之和,均作为特征变量,构建决策树回归算法模型。

import numpy as np

import pandas as pd

from tqdm import tqdm

import matplotlib.pyplot as plt

from sklearn.model_selection import train_test_split

from sklearn.model_selection import KFold

from sklearn.model_selection import GridSearchCV

from sklearn.tree import plot_tree

from sklearn.tree import DecisionTreeRegressor, export_text

from sklearn.linear_model import LinearRegression

1. 变量设置及数据处理

data = pd.read_csv("../data/数据4.3.csv")

data.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 8441 entries, 0 to 8440

Data columns (total 5 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 code 8441 non-null int64

1 Profit contribution 8441 non-null float64

2 Net interest income 8441 non-null float64

3 Intermediate income 8441 non-null float64

4 Deposit and finance daily 8441 non-null float64

dtypes: float64(4), int64(1)

memory usage: 329.9 KB

数据集包含8441条记录,5个字段,其中code为整数类型,其余4个为浮点数类型。所有字段均无缺失值。

data.isnull().values.any()

False

返回False表示数据集中不存在缺失值,数据完整性良好。

# 将样本示例全集分割为训练样本和测试样本

X = data.iloc[:, 1:] # 设置特征变量

y = data.iloc[:, 0] # 设置响应变量

X_train, X_test, y_train, y_test = train_test_split(

X, y, test_size=0.3, random_state=10

)

2. 未考虑成本-复杂度剪枝的决策树回归算法模型

model = DecisionTreeRegressor(max_depth=2, random_state=10)

model.fit(X_train, y_train)

print("拟合优度:", model.score(X_test, y_test))

拟合优度: 0.0357314987046895

未剪枝决策树模型在测试集上的R²值为0.0357,表明模型对数据的解释能力较弱。

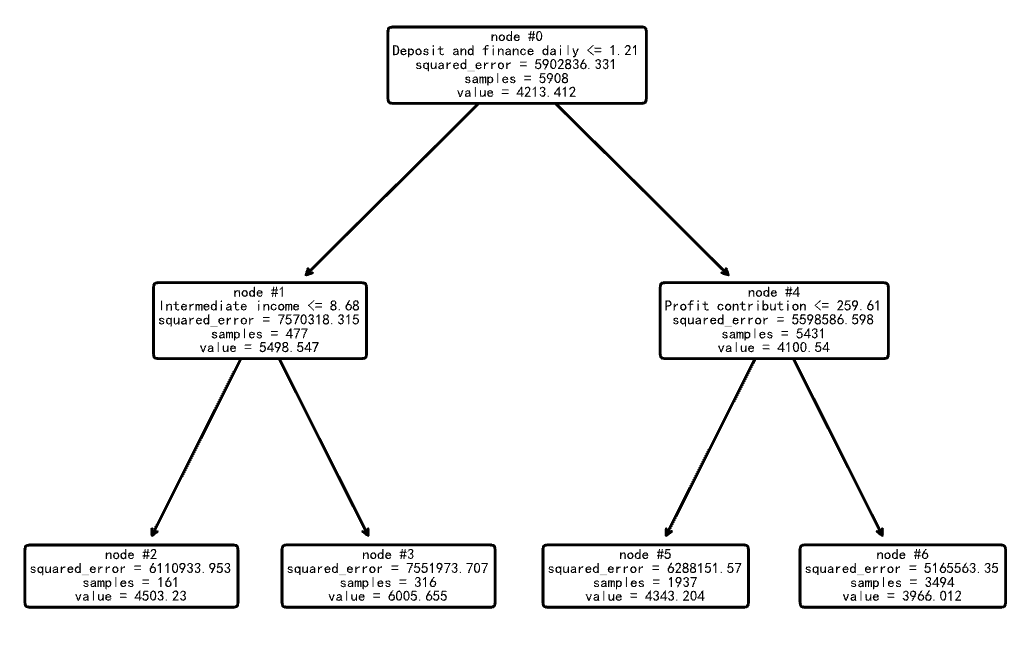

plot_tree(model, feature_names=X.columns, node_ids=True, rounded=True, precision=3)

plt.savefig("out1.pdf") # 有效解决显示不清晰的问题

print("文本格式的决策树:", export_text(model, feature_names=list(X.columns)))

文本格式的决策树: |--- Deposit and finance daily <= 1.21

| |--- Intermediate income <= 8.68

| | |--- value: [4503.23]

| |--- Intermediate income > 8.68

| | |--- value: [6005.66]

|--- Deposit and finance daily > 1.21

| |--- Profit contribution <= 259.61

| | |--- value: [4343.20]

| |--- Profit contribution > 259.61

| | |--- value: [3966.01]

深度为2的决策树首先根据”日均存款加理财之和”进行分裂,然后在各子节点中根据其他特征进一步分裂,最终生成4个叶节点,每个叶节点对应一个预测值。

3. 构建考虑成本-复杂度剪枝的决策树回归算法模型

model = DecisionTreeRegressor(random_state=10)

path = model.cost_complexity_pruning_path(X_train, y_train)

print("模型复杂度参数:", max(path.ccp_alphas)) # 输出最大的模型复杂度参数

print("模型总均方误差:", max(path.impurities)) # 输出最大的模型总均方误差

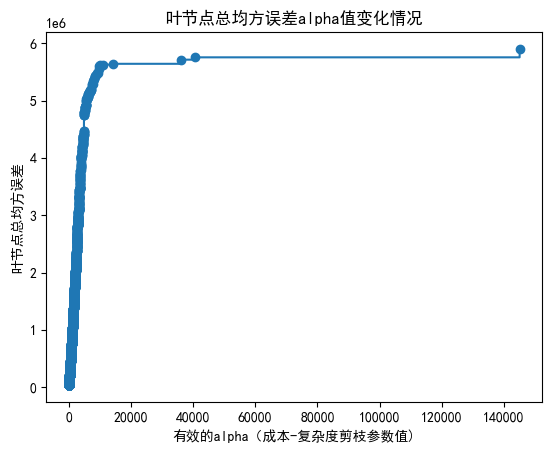

模型复杂度参数: 145056.0931541454

模型总均方误差: 5902836.331344441

最大的ccp_alpha值为145056.09,此时对应最大的模型总均方误差为5902836.33。这些值将用于后续剪枝过程中的参数选择。

4. 绘制图形观察”叶节点总均方误差随alpha值变化情况”

fig, ax = plt.subplots()

ax.plot(path.ccp_alphas, path.impurities, marker="o", drawstyle="steps-post")

ax.set_xlabel("有效的alpha(成本-复杂度剪枝参数值)")

ax.set_ylabel("叶节点总均方误差")

ax.set_title("叶节点总均方误差alpha值变化情况")

Text(0.5, 1.0, '叶节点总均方误差alpha值变化情况')

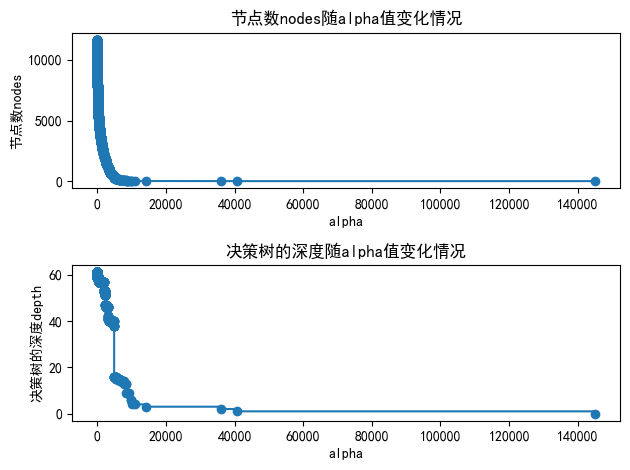

5. 绘制图形观察”节点数和树的深度随alpha值变化情况”

models = []

for ccp_alpha in tqdm(path.ccp_alphas):

model = DecisionTreeRegressor(random_state=10, ccp_alpha=ccp_alpha)

model.fit(X_train, y_train)

models.append(model)

print(

"最后一棵决策时的节点数为: {} ;其alpha值为: {}".format(

models[-1].tree_.node_count, path.ccp_alphas[-1]

)

) # 输出最path.ccp_alphas中最后一个值,即修剪整棵树的alpha值,只有一个节点

100%|██████████| 4643/4643 [11:00<00:00, 7.03it/s]

最后一棵决策时的节点数为: 1 ;其alpha值为: 145056.0931541454

成功训练了4643个不同alpha值的决策树模型,耗时约11分钟。当alpha取最大值145056.09时,决策树被剪枝为只有1个节点,即完全剪枝的状态。

node_counts = [model.tree_.node_count for model in models]

depth = [model.tree_.max_depth for model in models]

fig, ax = plt.subplots(2, 1)

ax[0].plot(path.ccp_alphas, node_counts, marker="o", drawstyle="steps-post")

ax[0].set_xlabel("alpha")

ax[0].set_ylabel("节点数nodes")

ax[0].set_title("节点数nodes随alpha值变化情况")

ax[1].plot(path.ccp_alphas, depth, marker="o", drawstyle="steps-post")

ax[1].set_xlabel("alpha")

ax[1].set_ylabel("决策树的深度depth")

ax[1].set_title("决策树的深度随alpha值变化情况")

fig.tight_layout()

6. 绘制图形观察”训练样本和测试样本的拟合优度随alpha值变化情况”

train_scores = [model.score(X_train, y_train) for model in models]

test_scores = [model.score(X_test, y_test) for model in models]

fig, ax = plt.subplots()

ax.set_xlabel("alpha")

ax.set_ylabel("拟合优度")

ax.set_title("训练样本和测试样本的拟合优度随alpha值变化情况")

ax.plot(

path.ccp_alphas, train_scores, marker="o", label="训练样本", drawstyle="steps-post"

)

ax.plot(

path.ccp_alphas, test_scores, marker="o", label="测试样本", drawstyle="steps-post"

)

ax.legend()

plt.show()

7. 通过10折交叉验证法寻求最优alpha值并开展特征变量重要性水平分析

7.1 通过10折交叉验证法寻求最优alpha值

param_grid = {"ccp_alpha": path.ccp_alphas}

kfold = KFold(n_splits=10, shuffle=True, random_state=10)

model = GridSearchCV(DecisionTreeRegressor(random_state=10),

param_grid,

cv=kfold,

n_jobs=-1) # 使用所有可用CPU核心

model.fit(X_train, y_train)

print("最优alpha值:", model.best_params_)

最优alpha值: {'ccp_alpha': 14222.786552228266}

通过10折交叉验证找到的最优alpha值为14222.79,该值将用于构建最终的决策树模型。

model = model.best_estimator_

print("最优拟合优度:", model.score(X_test, y_test))

print("决策树深度:", model.get_depth())

print("叶节点数目:", model.get_n_leaves())

print("每个变量的重要性:", model.feature_importances_)

最优拟合优度: 0.03600534073366668

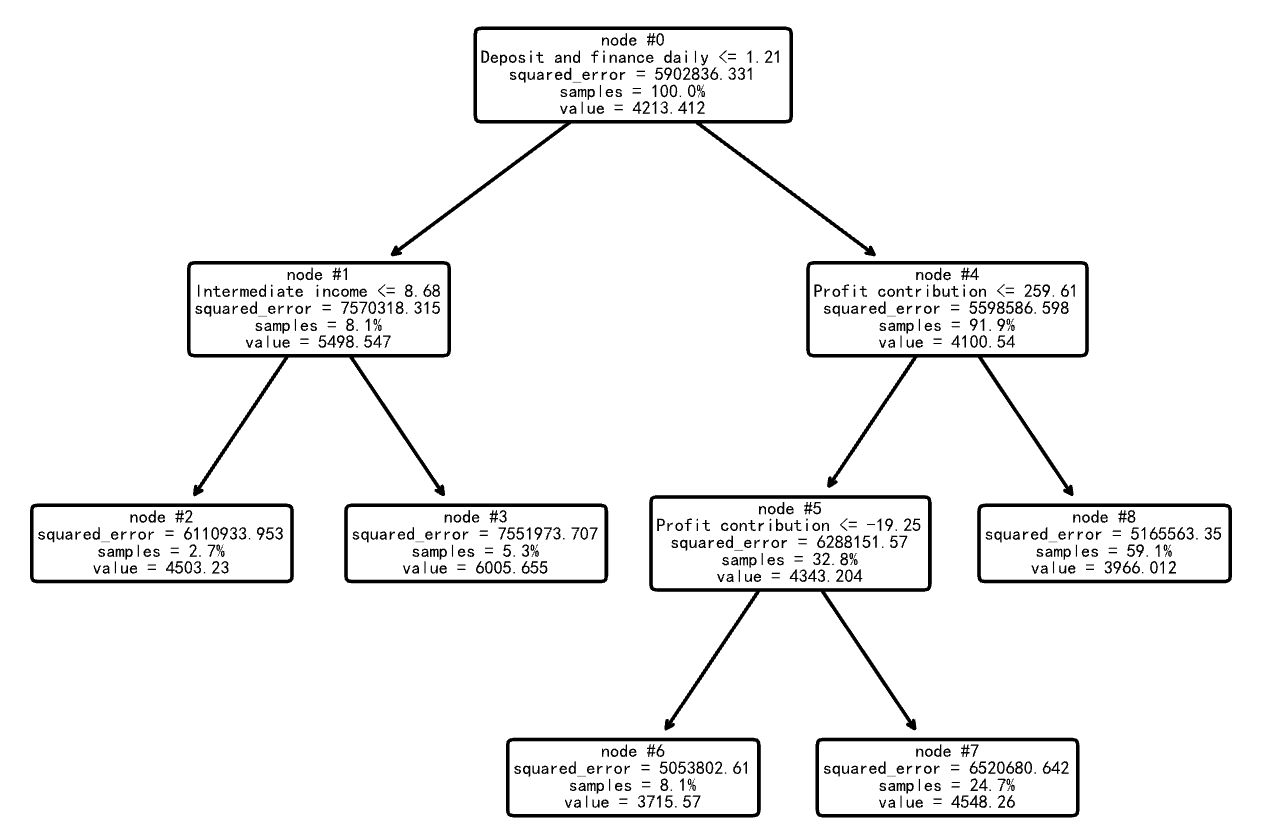

决策树深度: 3

叶节点数目: 5

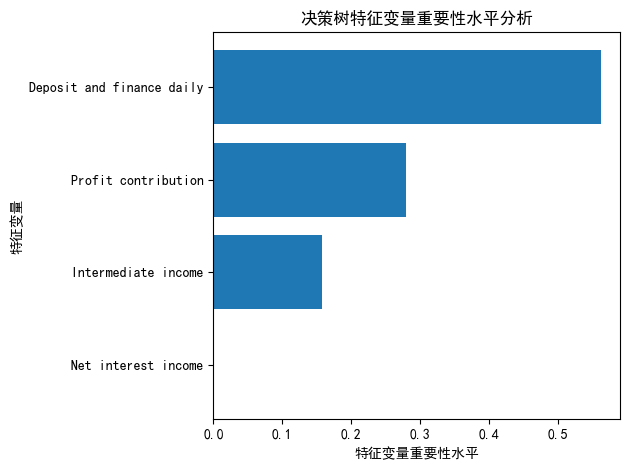

每个变量的重要性: [0.27985142 0. 0.15794261 0.56220597]

最优模型性能分析:

- 拟合优度R²值为0.0360,略高于未剪枝模型

- 决策树深度为3,包含5个叶节点

- 特征重要性显示:”日均存款加理财之和”(0.562)最重要,其次是”Profit contribution”(0.280)和”Intermediate income”(0.158),而”Net interest income”的重要性为0。

7.2 决策树特征变量重要性水平分析

sorted_index = model.feature_importances_.argsort()

plt.barh(range(X_train.shape[1]), model.feature_importances_[sorted_index])

plt.yticks(np.arange(X_train.shape[1]), X_train.columns[sorted_index])

plt.xlabel("特征变量重要性水平")

plt.ylabel("特征变量")

plt.title("决策树特征变量重要性水平分析")

plt.tight_layout()

plot_tree(

model,

feature_names=X.columns,

node_ids=True,

impurity=True,

proportion=True,

rounded=True,

precision=3,

)

plt.savefig("out2.pdf")

8. 最优模型拟合效果图形展示

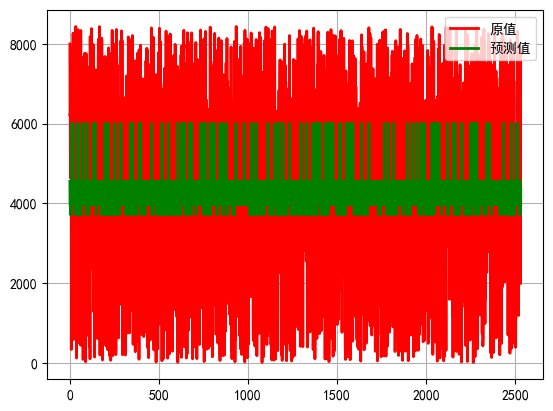

pred = model.predict(X_test) # 对响应变量进行预测

t = np.arange(len(y_test)) # 求得响应变量在测试样本中的个数,以便绘制图形。

plt.plot(t, y_test, "r-", linewidth=2, label="原值") # 绘制响应变量原值曲线。

plt.plot(t, pred, "g-", linewidth=2, label="预测值") # 绘制响应变量预测曲线。

plt.legend(loc="upper right") # 将图例放在图的右上方。

plt.grid()

plt.show()

9. 构建线性回归算法模型进行对比

model = LinearRegression().fit(X_train, y_train)

model.score(X_test, y_test)

4.4562697989802835e-05

线性回归模型的R²值为4.46×10⁻⁵,远低于决策树模型,表明在这个问题上,决策树回归算法表现优于线性回归算法。